Why Waiting for RSI Confirmation Is Costing You Money: 25 Years of Nasdaq 100 Data

Most traders wait for the RSI to turn back up before buying. Wait for the bounce. Wait for the confirmation. It sounds reasonable. Twenty five years of data across the entire Nasdaq 100 says it is leaving money on the table in almost every situation you can test.

Waiting for confirmation is one of the most repeated pieces of trading advice out there. The data disagrees with it pretty consistently. But before we get to the numbers, the way you test this question matters. A sloppy comparison produces a misleading answer. So let me walk you through exactly how this was set up and why.

All testing was done in Wealth-Lab using WealthData, the platform’s built in daily bar data. It is a clean data source checked for bad ticks and data oddities. That matters more than most people realize. Garbage data produces garbage results regardless of how good your system logic is.

The universe is Nasdaq 100 stocks over 25 years. The filter is straightforward. The 20 day moving average above the 50, the 50 above the 200, and SPY above its 200 day moving average. A setup most traders recognize immediately. Entry is at the open the morning after the signal fires. Fixed 5 day hold.

These are not obscure names. We are talking about stocks like NVDA, AMZN, and TSLA. Names that dominate trading forums, social media, and every watchlist worth looking at. The same stocks where most traders are waiting for that RSI crossover confirmation before pulling the trigger.

Now here is where the test design gets important. I used a 7 period RSI and tested every 5 point increment across the full RSI range. For each zone I created two mirror entries that both land in exactly the same place.

Take the 25 to 30 zone as an example. The cross under entry triggers when the RSI crosses down through 30 and closes above 25. The RSI fell into that zone on a down day. The cross over entry triggers when the RSI crosses up through 25 and closes below 30. The RSI rose into that zone on an up day.

Same zone. Same stocks. Same alignment. Same hold period. The only difference is the direction the RSI was traveling when it got there.

That is the cleanest possible apples to apples comparison for this question.

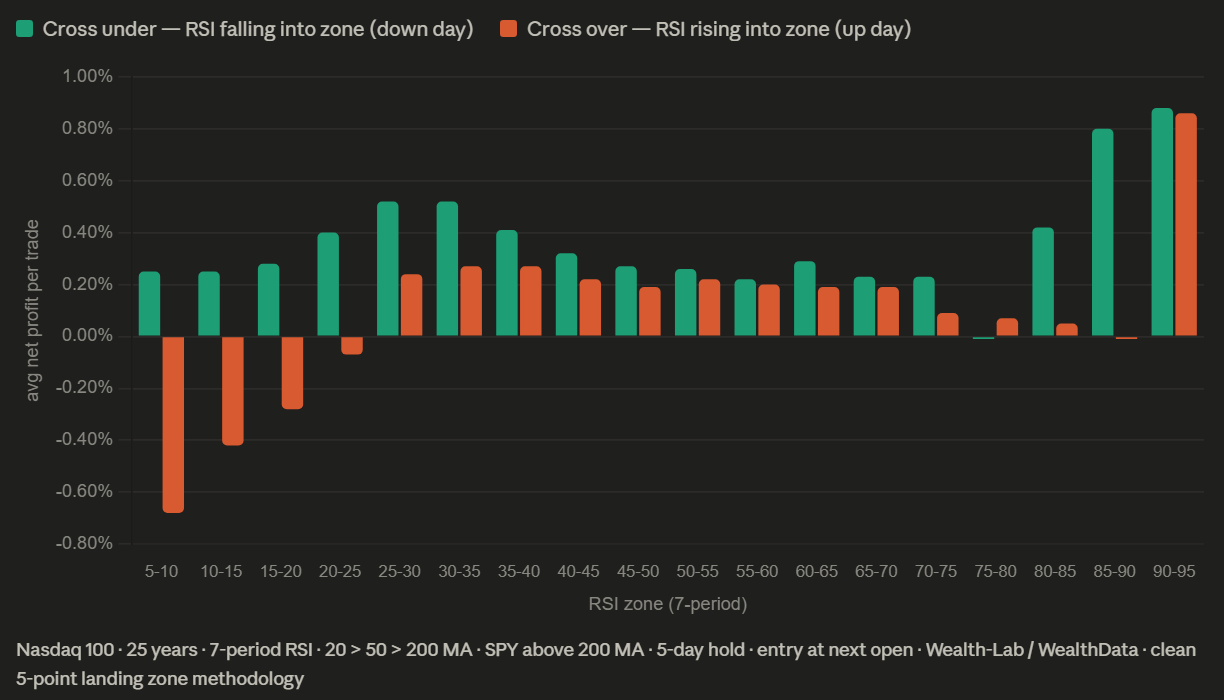

In 17 out of 18 zones tested buying into the falling RSI outperformed waiting for it to turn back up. One exception at the 75 to 80 zone where cross over edges cross under by 0.08%. Both approaches are marginal there anyway. That is not a meaningful win for confirmation. It is noise.

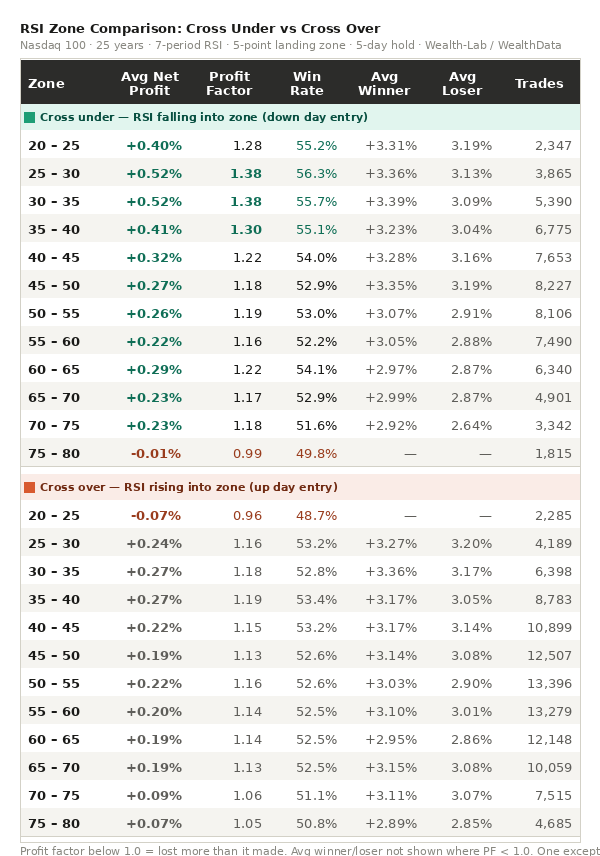

Take the 25 to 30 zone as one example. Buying the cross under produced an average net profit of 0.52%, a profit factor of 1.38, and a win rate of 56.25% across 3,865 trades. Waiting for confirmation in that same zone produced an average net profit of 0.24%, a profit factor of 1.16, and a win rate of 53.19% across 4,189 trades. Both entries profitable but cross under meaningfully better on every metric.

The low RSI zones tell the most dramatic story. In the 15 to 20 zone cross under delivers a profit factor of 1.20 with a win rate of 54.84%. Cross over in the same zone delivers a profit factor of 0.83 and a win rate of 46.89%. Below 1.0 on profit factor means the strategy lost more than it made. In a fully bullish aligned market, waiting for confirmation in a low RSI zone is a losing approach. The data is pretty clear on that.

Think about what these two entries actually look like on a chart. A cross under entry is a down day. Price is falling. It feels uncomfortable. A cross over entry is an up day. Price is rising. It feels safe. That up day is what is eating into your return. By the time the RSI turns back up the stock has already moved. The early money is already in.

Ask yourself why that up day printed. Someone bought the weakness before you did. While most traders were waiting for confirmation, other participants were already entering on the down day. By the time the RSI turns back up those buyers are already sitting on a profit. You are not getting confirmation. You are getting their exit.

The charts below show the full picture across all 18 zones. Take a minute to look at them before reading on. The pattern is hard to miss.

A quick note on what you are looking at. Profit factor measures how many dollars were won for every dollar lost across all trades in that zone. Above 1.0 the winning side outweighed the losing side. Below 1.0 means the strategy lost more than it made. That is the number to focus on.

[Visual 1 - avg net profit bar chart]

[Visual 2 - profit factor with breakeven line]

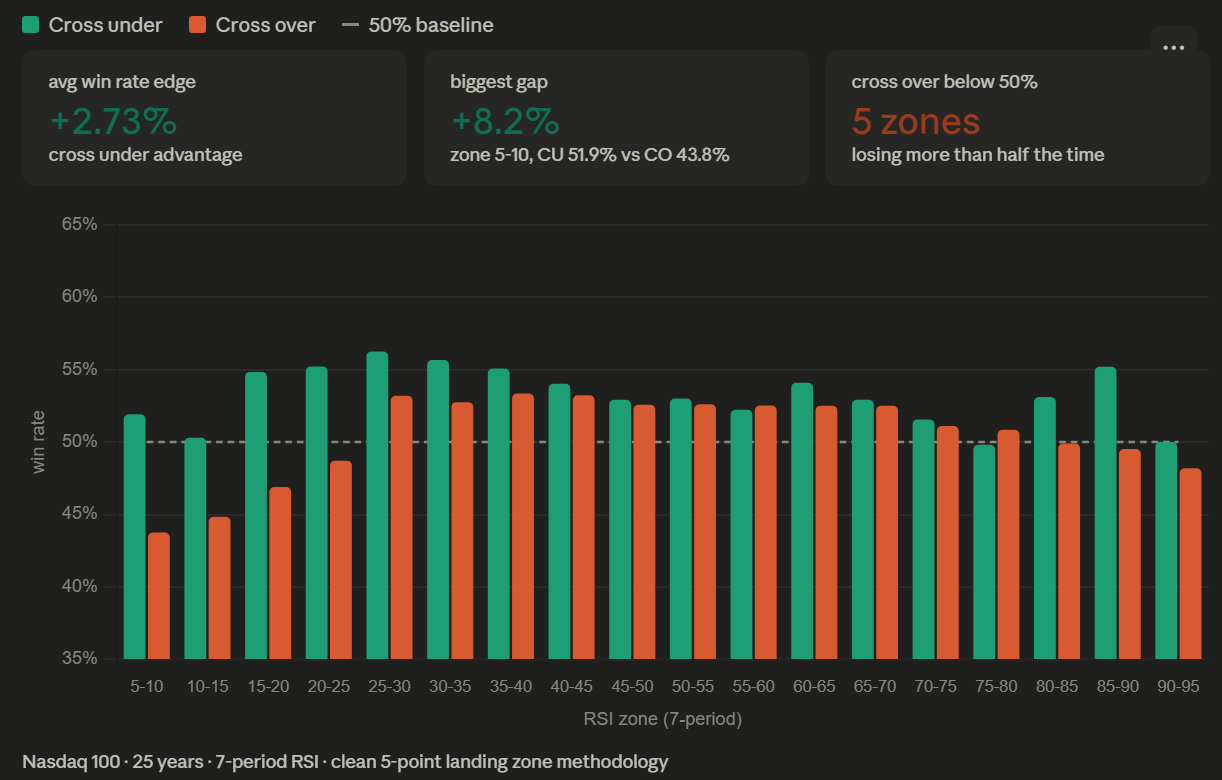

[Visual 3 - win rate]

[Visual 4 - full metrics table PNG]

A few things worth calling out. Cross over produces a profit factor below 1.0 in five zones. That means a losing strategy in five separate RSI zones within a fully bullish aligned market. Cross under produces a profit factor below 1.0 in exactly one zone, the 75 to 80 band, and even there the difference is marginal. Cross under wins 17 of 18 zones. The average win rate advantage across all zones is 2.73 percentage points. In the 25 to 30 and 30 to 35 zones cross under generates roughly twice the per trade return of cross over across thousands of trades. These are not small sample flukes.

Think about what these two entries actually look like on a chart. A cross under entry is a down day. Price is falling. It feels uncomfortable. A cross over entry is an up day. Price is rising. It feels like the right time to buy.

That up day is what is eating into your return. By the time the RSI turns back up the stock has already moved. The early money is already in.

Ask yourself why that up day printed. Someone bought the weakness before you did. While most traders were waiting for confirmation, other participants were already entering on the down day. By the time the RSI turns back up those buyers are already sitting on a profit. You are not getting confirmation. You are getting their exit.

This shows up in the data pretty clearly. In the lower RSI zones the cross over win rate drops below 50% in several bands. That means the confirmation entry is losing more than half its trades in zones where cross under is winning 54 to 56% of the time. Same zone. Same stocks. The difference is who got there first.

One more thing worth noting. I ran the same test using the standard 14 period RSI that most traders and most platforms default to. The result was the same. Cross under outperformed cross over in every comparable zone tested. The finding is not a function of using a faster RSI setting. It holds on the default that most traders are already using. Down is better than up regardless of which RSI period you prefer.

There is another way to think about these zones beyond pure edge quality. Sometimes you want more exposure in a strong market and you need a reason to pull the trigger. A trade with a documented edge in a bullish aligned stock can accomplish both things at once. You are not just taking a trade. You are adding exposure in a disciplined way that the data supports. That is worth something to a trader who wants to be in the market but does not want to chase.

What you have seen here is raw research. Not a trading system. A complete system requires position sizing, stop methodology, how to handle multiple signals on the same day, portfolio heat management, and whether 5 days is actually the right hold or just a reasonable starting point. None of that is resolved here.

What is resolved is a specific question about entry timing that most traders have never tested with clean methodology. In a bullish aligned Nasdaq 100 stock, buying weakness on a down day outperforms waiting for confirmation on an up day in 17 of 18 RSI zones tested. Across 25 years of data. With a methodology designed specifically to make the comparison fair.

The edge is not dramatic on any single trade. But staying consistently on the correct side of a structural finding like this across hundreds or thousands of trades over time adds up. That is how systematic trading works.

Would you rather know this than not? After 25 years of doing this kind of work I have never once wished I knew less.

If you want to see what this kind of research looks like when it has been developed into a complete tradeable system, that work is at tradingtimemachine.com.

Next up: the same test with a partial bullish alignment. The 20 has crossed under the 50 but the 50 is still above the 200. Does the edge survive when conditions start to deteriorate? The data will tell us.

Have a Great Night!

Dave Johnson

P.S. A quick note for those who follow along regularly. The pace of publishing has been slower than usual lately. We are in the middle of selling the house and preparing for a move to Italy. The house has a buyer and things are moving in the right direction. If all goes well I should have feet on the ground in Italy by early July. Looking forward to getting back to a more regular publishing schedule once the dust settles. Appreciate the patience.

This is a fascinating study. Thanks for sharing